Quick Summary

- Federal student loans usually cannot be negotiated like private loans.

- However, settlement is possible through compromise, forgiveness, or repayment programs.

- Income-driven repayment (IDR) plans can reduce monthly payments drastically.

- Defaulted loans may qualify for settlement through a collections compromise.

- Best strategy: Compare settlement vs forgiveness before choosing.

How to settle federal student loans?

Federal student loans can be settled by enrolling in income-driven repayment plans, applying for forgiveness programs, or negotiating a compromise settlement if the loan is in default. Each option depends on income, loan status, and eligibility.

If you’re overwhelmed by federal student loan debt in the U.S., you’re not alone. Millions of borrowers struggle with repayment every year, especially when interest keeps growing. The good news? Federal student loans offer several legal settlement pathways that can reduce or eliminate your balance over time.

Before diving in, you may want to review this foundational guide:

What is a student loan? — Understand loan types and structures first.

Can You Settle Federal Student Loans for Less Than You Owe?

Yes, but only in limited cases such as defaulted loans through a federal compromise settlement program.

Federal student loans are owned by the U.S. government, meaning they cannot be negotiated freely like private loans. However, there are three official settlement pathways:

1. Compromise Settlement (Defaulted Loans Only)

This applies when your loan is already in default and sent to collections.

You may negotiate:

- Waiver of collection fees

- Reduction in accrued interest

- Partial principal settlement (rare)

2. Forgiveness Programs

Instead of settlement, many borrowers reduce their balance legally through forgiveness options like:

- Public Service Loan Forgiveness (PSLF)

- Teacher Loan Forgiveness

- IDR forgiveness after 20–25 years

3. Repayment Plan Optimization

Income-driven repayment can lower monthly payments to $0–$50 based on income.

Comparison Table:

| Option | Settlement Amount | Eligibility | Long-Term Impact |

| Compromise Settlement | Reduced payoff | Defaulted loans | Debt closed faster |

| IDR Plans | Lower monthly payment | Low income | Forgiveness later |

| PSLF | Full forgiveness | Public service workers | No tax liability |

In short, federal loans aren’t easily negotiable, but strategic programs can significantly reduce or eliminate what you owe.

What Is the Federal Student Loan Compromise Program?

It allows defaulted federal loans to be settled for less than the full balance through a negotiated agreement with the Department of Education.

When federal loans go into default (270+ days past due), they may be assigned to collection agencies. At this stage, borrowers can request a compromise settlement.

Types of Federal Loan Settlements

- Principal + Interest Full Payment Waiver of Fees

- Principal + Half Interest Payment

- Negotiated Lump-Sum Settlement (rare)

According to the official U.S. Department of Education repayment plans, borrowers should first explore affordable repayment options before settlement.

Explore federal repayment plans

So the bottom line is: compromise settlements are mainly available only after default and typically require a lump-sum payment.

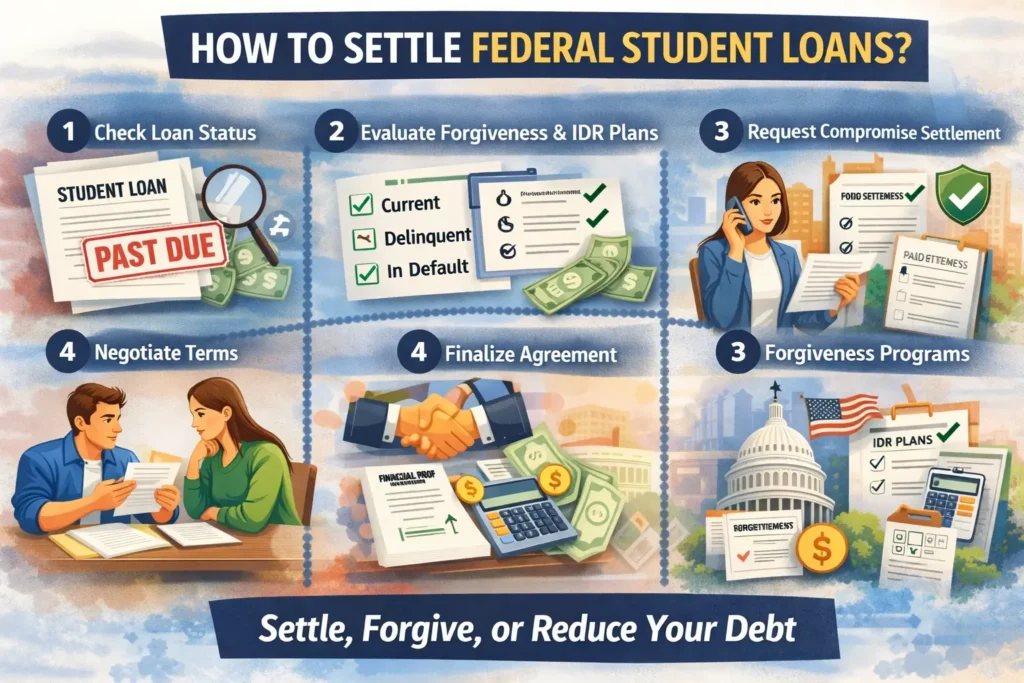

How to Settle Federal Student Loans Step-by-Step

Settlement involves checking loan status, evaluating repayment options, requesting compromise terms, and finalizing an agreement with the loan servicer.

Step 1: Check Loan Status

Determine whether your loan is:

- Current

- Delinquent

- In default

Learn more about collections here:

How student loans are collected

Step 2: Evaluate Forgiveness & IDR Plans

Before settlement, compare repayment strategies like:

Income-driven repayment (IDR) plans explained

Step 3: Request Compromise Settlement

Contact your loan servicer or collection agency and submit:

- Financial hardship proof

- Income documents

- Settlement proposal letter

Step 4: Negotiate Terms

You may negotiate:

- Interest reduction

- Fee waivers

- Partial balance payoff

Step 5: Finalize Written Agreement

Never pay without a signed written settlement confirmation.

Here’s what matters: verify loan status first, explore IDR or forgiveness, and only then negotiate settlement if the loan is in default.

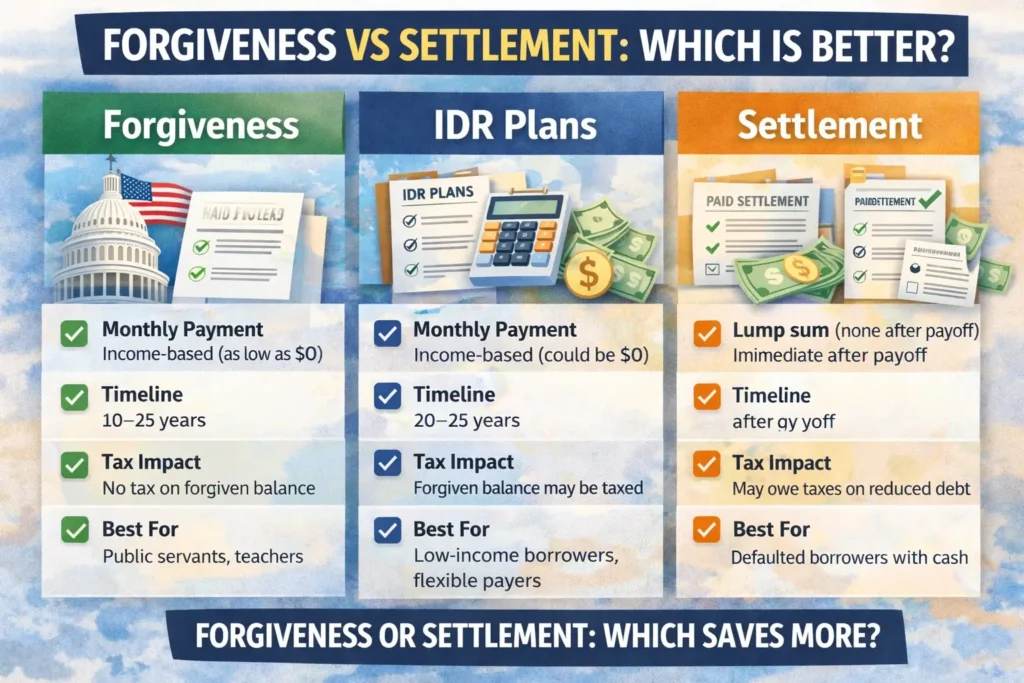

Settlement vs Forgiveness vs Repayment — Which Is Better?

Forgiveness is often better long-term, while settlement may be faster but requires a lump-sum payment.

Comparison Table

| Factor | Settlement | Forgiveness | IDR Plans |

| Monthly Payment | None after payoff | Based on income | Low payment |

| Time | Immediate | 10–25 years | Ongoing |

| Credit Impact | Neutral/Negative | Positive | Positive |

| Best For | Defaulted borrowers | Public workers | Low-income borrowers |

In short, forgiveness usually offers the best financial outcome, while settlement is useful if you want a faster debt closure.

Is Settling Federal Student Loans a Good Idea?

Settlement is helpful mainly for defaulted loans, but may not be ideal for active loans due to lost forgiveness benefits.

Pros:

- Faster debt resolution

- Reduced the balance possibility

- Stops collection actions

Cons:

- Requires a lump sum

- May impact credit history

- Forgiveness eligibility may be lost

For deeper comparison:

Federal vs private student loans differences

So the bottom line is: settlement can help in severe default situations, but isn’t always the best strategy for active loans.

How Much Can You Save by Settling Federal Student Loans?

Savings vary, but borrowers may reduce fees and interest, though principal reduction is less common.

Typical compromise savings:

- 100% collection fee removal

- 30–50% interest reduction

- Rare partial principal settlement

Example:

Loan Balance: $40,000

Settlement Offer: $28,000 lump sum

Savings: $12,000

Here’s what matters: most savings come from waived fees and reduced interest rather than large principal cuts.

Alternatives to Federal Student Loan Settlement

Alternatives include rehabilitation, consolidation, IDR plans, and bankruptcy adversary proceedings.

H3: 1. Loan Rehabilitation

Restores the loan to good standing after 9 on-time payments.

H3: 2. Loan Consolidation

Combines loans into one lower-payment plan.

H3: 3. Bankruptcy Discharge (Rare)

Learn the step-by-step process:

Student loan bankruptcy process

Also, explore the legal route:

How to file an adversary proceeding

In short, settlement is only one path; rehabilitation or IDR often provides safer long-term benefits.

As an SEO researcher working closely with U.S. federal loan policies, we’ve seen borrowers save thousands by switching from settlement attempts to IDR plans first. Real-life cases show that monthly payment reductions often outperform lump-sum settlements financially.

FAQ Section

Can federal student loans be negotiated?

Federal loans cannot be freely negotiated but may be settled through compromise if in default.

Will the settlement hurt my credit?

Yes, a settlement may appear as “paid less than owed,” slightly impacting the credit score.

Do federal student loans accept lump-sum settlements?

Yes, mainly after default, and usually require full principal plus partial interest.

Is forgiveness better than settlement?

Forgiveness is often better because it may eliminate the full balance without a lump-sum payment.

Can I settle federal loans while in school?

No, settlement is typically available only after default or severe delinquency.

Final Takeaway

If you’re struggling with federal student loan debt, the smartest approach is:

1️⃣ Check your repayment eligibility

2️⃣ Explore forgiveness programs

3️⃣ Consider settlement only if in default

For personalized guidance or consultation, visit:

Contact our student loan help team

Or explore the full hub resource:

Federal Student Loan Debt Home Guide