Summary of This Guide

- PSLF forgives the remaining federal student loan balance after 120 qualifying payments

- Must work for a government or nonprofit employer

- Loans must be Direct Loans

- Must enroll in an Income-Driven Repayment (IDR) plan

- Proper documentation & employment certification are crucial

What is Public Service Loan Forgiveness (PSLF)?

Public Service Loan Forgiveness (PSLF) is a U.S. federal program that forgives the remaining balance on Direct student loans after 120 qualifying monthly payments while working full-time for a government or eligible nonprofit employer.

If you’re struggling with federal student debt, PSLF can eliminate your remaining loan balance tax-free after 10 years of qualifying payments.

To understand loan basics first, read: beginner’s guide to student loans

Additionally, for complete student loan insights, visit the official student loan debt assistance hub

PSLF refers to a federal forgiveness initiative that rewards public service employees by canceling remaining federal student debt after qualifying repayment and employment requirements.

In short, PSLF is a government-backed forgiveness program designed for public service workers who make consistent payments for 10 years.

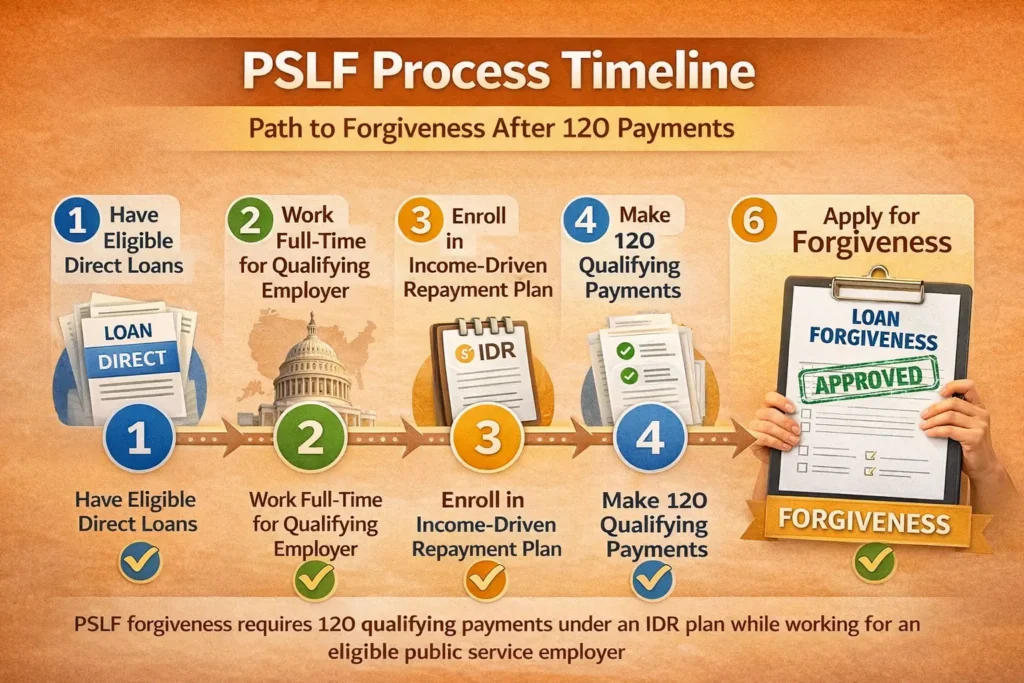

How Does PSLF Work Step by Step?

PSLF works by requiring 120 qualifying payments under an IDR plan while working full-time for an eligible employer.

Step-by-Step Process

- Have eligible Direct Loans

- Work full-time for a qualifying employer

- Enroll in an Income-Driven Repayment plan

- Make 120 qualifying monthly payments

- Submit PSLF Employment Certification Form

- Apply for forgiveness after 120 payments

For IDR plan understanding, see: IDR plans for federal student loans

PSLF Workflow Table

| Step | Requirement | Details |

| 1 | Eligible Loan | Direct Federal Loans only |

| 2 | Employer | Government or Nonprofit |

| 3 | Repayment Plan | IDR plan required |

| 4 | Payments | 120 qualifying payments |

| 5 | Certification | Annual employment verification |

| 6 | Forgiveness | Remaining balance forgiven |

Here’s what matters: PSLF requires disciplined repayment plus verified public service employment for 10 years.

Who Qualifies for Public Service Loan Forgiveness?

You qualify for PSLF if you work full-time for a government or 501(c)(3) nonprofit and have Direct Loans on an IDR plan.

Eligible Employers

- Federal, State, Local Government

- Public Schools & Universities

- 501(c)(3) Nonprofit Organizations

- Military service members

Ineligible Employers

- Private for-profit companies

- Labor unions

- Political organizations

Learn the federal vs private differences: the difference between federal and private loans

So the bottom line is: only public service and nonprofit employment qualify for PSLF forgiveness.

What Loans Are Eligible for PSLF?

Only Direct Loans qualify; FFEL and Perkins loans must be consolidated into a Direct Consolidation Loan.

Eligible Loans

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Direct PLUS Loans

- Direct Consolidation Loans

Non-Eligible Loans

- FFEL Loans

- Perkins Loans (unless consolidated)

- Private student loans

If you’re unsure about collections:

How Student Loans Are Collected

In short, PSLF applies strictly to federal Direct Loans — private loans never qualify.

How Many Payments Are Required for PSLF?

PSLF requires 120 qualifying monthly payments made under an IDR plan while employed by a qualified public service employer.

What Counts as a Qualifying Payment?

- On-time monthly payment

- Full scheduled payment amount

- Paid under a qualifying repayment plan

- While employed full-time

What Does NOT Count?

- Late payments

- Partial payments

- Payments during forbearance or deferment

Here’s what matters: 120 on-time payments under the correct plan are mandatory for forgiveness.

PSLF vs IDR Forgiveness Comparison

| Feature | PSLF | IDR Forgiveness |

| Time Required | 10 Years | 20–25 Years |

| Employer Requirement | Yes | No |

| Tax on Forgiveness | No | Yes (usually) |

| Payment Plan | IDR Required | IDR Required |

| Loan Type | Direct Loans Only | Most federal loans |

PSLF is faster and tax-free, while IDR forgiveness takes longer but doesn’t require public service employment.

Can PSLF Be Denied?

Yes, PSLF can be denied if payments, employment, or loan types do not meet strict program requirements.

Common PSLF Rejection Reasons

- Wrong repayment plan

- Ineligible employer

- Missing certification forms

- Loan not consolidated into a Direct Loan

If considering alternatives: negotiating private student loan debt

So the bottom line is: most PSLF denials happen due to documentation or eligibility errors.

How to Apply for Public Service Loan Forgiveness

Apply by submitting PSLF Employment Certification annually and final forgiveness application after 120 payments.

Application Steps

- Work for a qualifying employer

- Enroll in the IDR plan

- Submit the Employment Certification Form yearly

- Track qualifying payments

- Apply after 120 payments

For legal hardship cases:

How to File an Adversary Proceeding

In short, consistent certification and accurate payment tracking are key to PSLF approval.

PSLF Timeline: How Long Does It Take?

PSLF forgiveness takes at least 10 years because borrowers must complete 120 qualifying monthly payments.

Timeline Breakdown

- Year 1–10: Make qualifying payments

- Annual: Submit employment certification

- After Payment 120: Apply for forgiveness

- Processing Time: 3–6 months average

Here’s what matters: PSLF is a long-term strategy that rewards consistent repayment discipline.

Is Public Service Loan Forgiveness Worth It in 2026?

PSLF is worth it for borrowers with high federal student loan balances working in long-term public service careers.

When PSLF Makes Sense

- High loan balance ($50k+)

- Low to moderate income

- Long-term nonprofit or government career

When PSLF May Not Be Ideal

- Switching to the private sector soon

- Low remaining loan balance

- Ineligible loan types

If bankruptcy is being considered: student loan bankruptcy process step by step

So the bottom line is: PSLF is most valuable for long-term public servants with significant federal loan debt.

For official historical background and policy details, see: Public Service Loan Forgiveness program overview

Final Takeaway

Public Service Loan Forgiveness is one of the most powerful federal student loan relief programs available in 2026. By working in public service and making 120 qualifying payments under an IDR plan, borrowers can receive full tax-free loan forgiveness.

If you need personalized eligibility guidance, get personalized student loan forgiveness help

FAQ – Public Service Loan Forgiveness

1. What is PSLF in simple terms?

PSLF is a federal program that forgives student loan balances after 120 qualifying payments while working in public service.

2. Do I need to work 10 years continuously?

No. Payments can be non-consecutive but must total 120 qualifying months.

3. Does PSLF forgive private student loans?

No. PSLF only applies to federal Direct Loans.

4. Can I lose PSLF eligibility?

Yes. Changing to an ineligible employer or repayment plan can stop qualifying payments.

5. Is PSLF forgiveness taxable?

No. PSLF forgiveness is completely tax-free under current federal law.

6. Is PSLF guaranteed after 120 payments?

Not automatically. You must apply and confirm that all eligibility criteria are met.

7. What happens if my application is denied?

You can correct errors, consolidate loans, or continue qualifying payments and reapply.