Quick Summary

- Yes, federal student loans can be forgiven after 20 years under Income-Driven Repayment (IDR) plans.

- Only Direct federal loans qualify for 20-year forgiveness.

- Some plans require 25 years, depending onthe loan type and repayment plan.

- Forgiveness happens after qualifying monthly payments, not simply time passing.

- Tax treatment may apply depending on current US federal law.

Can federal loans be forgiven after 20 years?

Yes. Federal student loans can be forgiven after 20 years if you are enrolled in an Income-Driven Repayment (IDR) plan and make qualifying monthly payments. Eligibility depends on loan type, repayment plan, and consistent repayment history in the United States.

Why This Question Matters in 2026

Student loan borrowers across the United States often wonder whether their federal loans will eventually disappear after years of payments. The 20-year forgiveness rule is real—but misunderstood.

Many borrowers assume forgiveness is automatic. In reality, forgiveness depends on enrollment in qualifying repayment programs and consistent payments.

If you’ve ever struggled with rising balances, you’re not alone. Loan interest, repayment plans, and policy changes make forgiveness rules confusing. You can explore foundational insights in this pillar resource: Federal Student Loan Debt Help Guide

Understanding how forgiveness works helps you avoid costly mistakes and choose the best repayment strategy.

What Does “Federal Loan Forgiveness After 20 Years” Actually Mean?

Federal loan forgiveness after 20 years means the remaining loan balance is canceled after qualifying payments under approved income-driven repayment plans.

Federal loan forgiveness after 20 years refers to a policy where eligible borrowers on Income-Driven Repayment (IDR) plans may have their remaining loan balance canceled after making qualifying monthly payments for 20 years (240 payments).

However, this forgiveness is not automatic just because 20 calendar years pass.

Instead, borrowers must:

- Be enrolled in a qualifying IDR plan

- Make consistent monthly payments

- Maintain eligible federal Direct Loans

- Avoid long periods of deferment or default

Federal loan forgiveness after 20 years is a benefit under income-driven repayment plans, where remaining federal student loan debt is canceled after 240 qualifying payments based on income and family size.

In short, forgiveness is tied to qualifying payments—not just time. Staying enrolled in IDR plans is essential to reach cancellation eligibility.

Which Federal Student Loans Qualify for 20-Year Forgiveness?

Only Direct federal student loans qualify for 20-year IDR forgiveness; older FFEL or Perkins loans require consolidation to qualify.

Not all federal loans qualify automatically. Loan type determines whether you can receive forgiveness after 20 years.

Eligible Loan Types

| Loan Type | Eligible for 20-Year Forgiveness? | Notes |

| Direct Subsidized Loans | Yes | Fully eligible under IDR |

| Direct Unsubsidized Loans | Yes | Qualifies under PAYE & REPAYE |

| Direct Consolidation Loans | Yes | Must include eligible loans |

| FFEL Loans | No (unless consolidated) | Must convert to Direct Loan |

| Perkins Loans | No (unless consolidated) | Needs Direct consolidation |

If you hold older federal loans, you may need consolidation before qualifying for forgiveness timelines.

For a deeper understanding of federal vs private eligibility differences, see: federal vs private student loans comparison guide

So the bottom line is: Only Direct Loans count automatically. Older loan programs must be consolidated to enter the 20-year forgiveness track.

How Do Income-Driven Repayment (IDR) Plans Lead to Forgiveness?

Income-driven repayment plans reduce monthly payments based on income and forgive the remaining balance after 20 or 25 years of qualifying payments.

Income-Driven Repayment (IDR) plans are the primary pathway to federal student loan forgiveness after long-term repayment.

These plans calculate monthly payments using:

- Adjusted Gross Income (AGI)

- Family size

- Federal poverty guidelines (USA)

Common IDR Plans include:

- PAYE (Pay As You Earn) – 20 years forgiveness

- IBR (Income-Based Repayment) – 20 or 25 years

- REPAYE / SAVE Plan – 20–25 years, depending on loan type

You can learn detailed plan mechanics here: Income-driven repayment plans explained

For official eligibility criteria and payment calculation rules, refer to: Official federal repayment plan guidelines

In short, IDR plans adjust payments based on income and eventually forgive the remaining balance after long-term qualifying payments.

Is Forgiveness Automatic After 20 Years of Payments?

No. Forgiveness is not automatic; borrowers must remain enrolled in an IDR plan and complete required qualifying payments.

One of the biggest misconceptions is that student loans automatically disappear after 20 years. That is not true.

Forgiveness requires:

- Continuous enrollment in an IDR plan

- Annual income recertification

- 240 qualifying monthly payments

- Loans in good standing (not defaulted)

Missed recertification or switching repayment plans can delay forgiveness eligibility.

Here’s what matters: Forgiveness happens only after verified qualifying payments, not simply because 20 years passed on the calendar.

What Happens If You Still Have a Balance After 20 Years?

If you still have a remaining balance after 20 years of qualifying IDR payments, that balance may be fully forgiven.

After reaching 240 qualifying payments, the Department of Education reviews your repayment history. If all conditions are met, any remaining loan balance—including unpaid interest—can be forgiven.

This often happens because IDR payments may be lower than interest accrual, causing balances to grow over time.

You can explore why balances increase despite payments here:

Why are student loans growing quickly in the United States

So the bottom line is: If qualifying payments are complete, the remaining loan balance may be canceled even if it has grown due to interest.

- Forgiveness after 20 years applies only to federal Direct Loans

- Enrollment in IDR plans is mandatory

- Payments must be qualifying monthly payments

- Balance remaining after the timeline can be canceled

- Missing recertification can delay forgiveness eligibility

Now that you understand the basic rule, the next critical step is learning the exact eligibility requirements, payment counting rules, and 20 vs 25-year forgiveness differences.

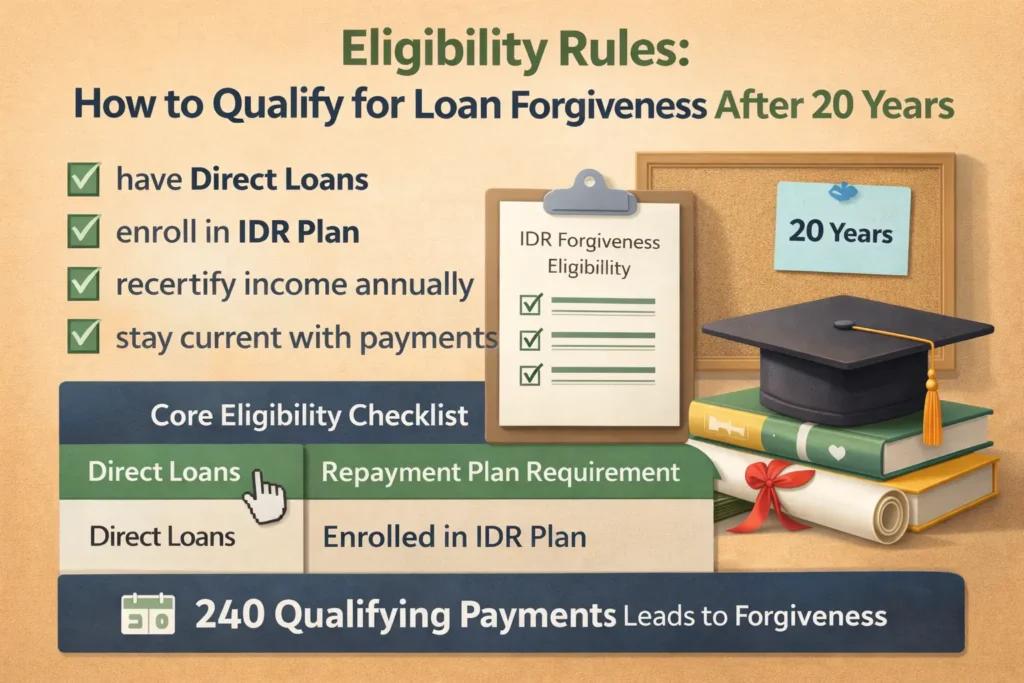

Who Qualifies for Federal Loan Forgiveness After 20 Years?

Borrowers qualify for 20-year federal loan forgiveness if they have Direct Loans, enroll in IDR plans, and make qualifying payments.

Understanding eligibility is crucial because not every borrower automatically qualifies for 20-year federal student loan forgiveness in the United States.

To be eligible, borrowers must meet specific federal requirements tied to loan type, repayment plan, and payment history.

Core Eligibility Checklist (IDR Forgiveness – USA)

You may qualify for forgiveness after 20 years if:

- You have Direct federal student loans

- You are enrolled in an Income-Driven Repayment (IDR) plan

- You make qualifying monthly payments

- You recertify income annually

- Your loans remain in good standing (not defaulted)

Borrowers unsure about the loan type can review eligibility through official federal guidelines here: Federal repayment plan eligibility rules

In short, eligibility depends on loan type, repayment plan enrollment, and consistent qualifying payments—not just loan age.

How Are Qualifying Payments Counted Toward 20-Year Forgiveness?

Qualifying payments are monthly payments made under an IDR plan while loans remain in active repayment status.

A major source of confusion borrowers face is how payments are counted. The 20-year rule is based on 240 qualifying monthly payments, not simply 20 calendar years.

What Counts as a Qualifying Payment?

A payment counts if:

- It is made under an IDR plan

- It is paid on time or within the allowed grace period

- The payment amount matches your approved IDR calculation

- The loan is not in default, deferment, or forbearance (with some exceptions)

What Does NOT Count?

- Payments made under Standard Repayment (unless later switched and credited under adjustments)

- Periods of default

- Long deferment without a qualifying status

- Missed income recertification periods

For borrowers struggling with complex repayment histories, seeking professional guidance can help: Student loan help consultation

Here’s what matters: Only verified IDR monthly payments count toward the 240-payment forgiveness timeline.

20-Year vs 25-Year Forgiveness: What’s the Difference?

Some IDR plans offer forgiveness after 20 years, while others require 25 years, depending on the loan type and repayment plan.

Not all income-driven repayment plans offer the same forgiveness timeline. Some plans require 20 years, while others extend to 25 years before cancellation eligibility.

Forgiveness Timeline Comparison Table

| Repayment Plan | Undergraduate Loans | Graduate Loans | Forgiveness Timeline |

| PAYE | Yes | No | 20 years |

| IBR (new borrowers) | Yes | Yes | 20 years |

| IBR (older borrowers) | Yes | Yes | 25 years |

| REPAYE / SAVE | Yes | Yes | 20–25 years, depending on loan mix |

This difference exists because graduate loans often carry larger balances and longer repayment structures.

So the bottom line is: Undergraduate borrowers often qualify for 20-year forgiveness, while graduate borrowers may need 25 years.

SAVE Plan vs PAYE: Which One Leads to Faster Forgiveness?

PAYE usually offers faster 20-year forgiveness, while SAVE may extend to 25 years, depending on graduate loan balance.

The SAVE Plan (formerly REPAYE) is now the most flexible income-driven repayment option in the United States. However, its forgiveness timeline varies depending on loan composition.

Key Differences Between SAVE and PAYE

| Feature | PAYE | SAVE Plan |

| Forgiveness Timeline | 20 years | 20–25 years |

| Income Protection | Moderate | Higher income protection |

| Payment Percentage | ~10% discretionary income | Often lower effective payments |

| Interest Benefit | Limited | Prevents unpaid interest growth |

Borrowers choosing between plans should consider whether they want lower monthly payments or a faster forgiveness timeline.

In short, PAYE may forgive loans faster, while SAVE can reduce payments and prevent balance growth during repayment.

Do Periods of Deferment or Forbearance Affect the 20-Year Timeline?

Yes. Long deferment or forbearance periods may pause qualifying payment counts and delay forgiveness eligibility.

Borrowers sometimes pause payments due to financial hardship, unemployment, or returning to school. However, these pauses can affect the 20-year forgiveness clock.

When Deferment May Count

- Certain economic hardship deferments (policy dependent)

- Government-approved pandemic payment pauses (special adjustments)

When It Usually Does NOT Count

- General voluntary forbearance

- Extended deferment without qualifying IDR status

- Loan default recovery periods

Borrowers with long deferment histories should review repayment adjustments carefully, especially when balances grow faster than expected: Why do loan balances increase over time

So the bottom line is: Pausing payments can delay forgiveness unless the period qualifies under specific federal adjustment programs.

Is Income Recertification Required Every Year?

Yes. Borrowers must recertify income annually to stay in IDR plans and continue counting payments toward forgiveness.

Annual income recertification ensures that your monthly payment accurately reflects your financial situation. Failing to recertify can increase payments and pause qualifying progress.

Recertification Impacts

- Keeps payment amount affordable

- Prevents removal from the IDR plan

- Ensures continued progress toward forgiveness

Here’s what matters: Missing recertification can interrupt your progress and delay 20-year forgiveness eligibility.

- Only Direct Loans qualify automatically for IDR forgiveness

- 240 qualifying monthly payments are required

- Some plans require 25 years instead of 20

- SAVE Plan may extend timeline for graduate loans

- Deferment and missed recertification can delay forgiveness

Pros and Cons of Federal Loan Forgiveness After 20 Years

20-year federal loan forgiveness offers long-term debt relief but may increase total interest paid and extend the repayment timeline significantly.

Choosing to pursue federal loan forgiveness after 20 years can be life-changing, but it also comes with trade-offs. Borrowers must evaluate both financial and psychological impacts before committing to long-term repayment strategies.

Major Benefits of 20-Year Federal Loan Forgiveness

1. Long-Term Debt Relief Protection

Income-Driven Repayment (IDR) plans ensure that borrowers never pay more than an affordable percentage of their income. This protects against financial hardship during unemployment, career transitions, or economic downturns in the United States.

2. Lower Monthly Payments Based on Income

IDR plans adjust payments using income and family size, making repayment manageable even with high loan balances.

This is particularly helpful if you experience fluctuating income, such as freelancing, gig work, or early-career salary growth.

3. Remaining Balance Can Be Fully Cancelled

After completing qualifying payments for 20 years, any remaining loan balance—including accumulated interest—may be forgiven under federal rules.

Understanding why balances grow over time can clarify this advantage: Why student loan balances grow over time

In short, the biggest benefit is guaranteed long-term protection—no matter how large the remaining loan balance becomes.

Potential Drawbacks and Risks of Waiting 20 Years

Waiting 20 years may increase total interest paid and create uncertainty due to future policy or tax law changes.

1. Total Interest Paid May Be Higher

Because IDR payments are often lower than standard repayment plans, unpaid interest can accumulate for many years. This may increase the overall cost before forgiveness is granted.

2. Forgiveness Depends on Policy Stability

Student loan policies evolve. Future legislative changes in the United States could modify forgiveness timelines, eligibility, or tax treatment.

3. Long-Term Psychological Debt Burden

Carrying debt for two decades can create mental stress and financial uncertainty, especially for borrowers planning major life decisions like buying a home.

So the bottom line is: Forgiveness provides relief but may cost more in interest and require patience for long-term repayment commitment.

Are Forgiven Student Loans Taxable After 20 Years?

Forgiven federal student loans may be taxable after 20 years, depending on current US federal tax laws and temporary policy provisions.

Tax implications are one of the most critical factors borrowers overlook when planning for loan forgiveness.

Current US Tax Treatment (2026 Context)

Under temporary federal law provisions, most forgiven student loan balances are not federally taxable through 2025. However, future tax treatment may change unless extended by legislation.

Possible Tax Scenarios

- Federal tax-free forgiveness (if current policies remain extended)

- Taxable forgiveness counted as income (if law expires)

- State tax rules may vary by location in the United States

Borrowers should consult tax professionals before final forgiveness to avoid unexpected tax liability.

Here’s what matters: Forgiveness may be tax-free now, but future tax rules could change—so long-term planning is essential.

Is Waiting 20 Years for Forgiveness Financially Worth It?

It depends on income growth, loan balance, and repayment plan; forgiveness benefits high-balance, low-income borrowers most.

Financial worth varies widely between borrowers. For some, forgiveness is the smartest strategy. For others, faster payoff or refinancing may save more money.

Cost-Benefit Comparison Table

| Scenario | Forgiveness Strategy | Faster Repayment Strategy |

| High loan balance, low income | Best option | Hard to manage payments |

| Rising career income | Moderate benefit | A faster payoff may save interest |

| Small loan balance | Not ideal | Paying off early is cheaper |

| Unstable employment | Very helpful | High risk of missed payments |

Borrowers unsure about long-term affordability can review full repayment strategies here: Income-driven repayment plan strategy guide

In short, forgiveness is most valuable for borrowers with large balances and lower long-term income growth expectations.

Forgiveness vs Refinancing vs Settlement: Which Is Better?

Forgiveness suits federal borrowers with low income, refinancing suits high earners, and settlement may help in severe hardship situations.

Borrowers often compare forgiveness with other debt-reduction strategies. Each approach serves a different financial situation.

Strategy Comparison Table

| Strategy | Best For | Key Advantage | Main Risk |

| IDR Forgiveness | Low-income borrowers | Balance cancellation | Long timeline |

| Refinancing | High-income professionals | Lower interest rates | Lose federal protections |

| Debt Settlement | Financial hardship cases | Reduce total payoff | Credit impact risk |

So the bottom line is: The best strategy depends on income stability, loan balance size, and long-term financial goals.

Psychological and Life Planning Considerations

Long-term forgiveness plans require emotional patience, stable income planning, and consistent repayment discipline over two decades.

Debt is not only financial—it also affects lifestyle decisions. Borrowers waiting 20 years for forgiveness often delay:

- Home ownership

- Business investment

- Career changes

- Retirement planning

However, IDR plans offer flexibility by adjusting payments during life transitions.

In short, forgiveness provides flexibility but requires long-term emotional and financial discipline.

- Forgiveness lowers the monthly payment burden long-term

- Total interest paid may increase over time

- Tax treatment depends on future US legislation

- High-balance borrowers benefit most financially

- Refinancing may be better for high-income earners

Alternatives to 20-Year Federal Loan Forgiveness: What Are Your Options?

Alternatives include Public Service Loan Forgiveness, refinancing, loan consolidation, or faster repayment strategies, depending on income and career path.

While federal loan forgiveness after 20 years is a powerful relief option, it is not the only path available to borrowers in the United States. Some alternatives may lead to faster debt freedom or lower overall cost.

Choosing the right strategy depends on:

- Career field

- Income growth potential

- Loan balance size

- Risk tolerance and financial goals

Public Service Loan Forgiveness (PSLF) vs 20-Year Forgiveness

PSLF forgives federal loans after 10 years of qualifying public service employment, making it faster than standard 20-year IDR forgiveness.

Public Service Loan Forgiveness (PSLF) is one of the most attractive alternatives to long-term forgiveness. Instead of waiting 20 years, eligible borrowers may receive forgiveness after only 120 qualifying payments (10 years).

PSLF vs IDR Forgiveness Comparison

| Feature | PSLF | 20-Year IDR Forgiveness |

| Forgiveness Timeline | 10 years | 20–25 years |

| Eligible Employment | Public service only | Any employment |

| Payment Plan | Must use IDR | IDR required |

| Tax Treatment | Tax-free federally | May be taxable (future dependent) |

| Flexibility | Limited to qualifying jobs | Flexible career choices |

PSLF is ideal for borrowers working in:

- Government jobs

- Non-profit organizations

- Public education or healthcare

However, if you plan to switch to private sector roles, long-term IDR forgiveness may be the more flexible option.

In short, PSLF offers faster forgiveness but requires strict employment eligibility, while 20-year forgiveness works regardless of career field.

Federal Loan Consolidation: Can It Help You Reach Forgiveness Faster?

Consolidation can make older federal loans eligible for IDR forgiveness, but it may reset payment counts if done incorrectly.

Loan consolidation combines multiple federal loans into a single Direct Consolidation Loan. This process is often necessary for borrowers with FFEL or Perkins loans that do not directly qualify for IDR forgiveness.

When Consolidation Helps

- You hold FFEL or Perkins loans

- You need access to SAVE, PAYE, or IBR plans

- You want a simplified single monthly payment

Potential Risks

- Payment count resets if not processed under the adjustment programs

- Longer repayment timeline if done late

- Loss of certain borrower benefits tied to the original loan

So the bottom line is: Consolidation can unlock forgiveness eligibility, but timing and processing rules are critical.

Refinancing Federal Student Loans: When Is It Better Than Forgiveness?

Refinancing may be better for high-income borrowers who can secure lower interest rates and plan to repay loans faster.

Refinancing replaces federal loans with a private loan at a new interest rate. While this can reduce interest costs, it removes federal protections, including IDR forgiveness eligibility.

When Refinancing Makes Sense

- Stable high income

- Low debt-to-income ratio

- Strong credit score

- Desire to pay off loans quickly

When Refinancing Is Risky

- Income instability

- Desire for forgiveness safety net

- Need for deferment or hardship protections

Here’s what matters: Refinancing can save interest but permanently removes access to federal forgiveness programs.

Student Loan Settlement: A Last-Resort Alternative?

Loan settlement may reduce the payoff amount, but it is typically risky and only suitable for borrowers facing severe financial hardship.

Debt settlement involves negotiating a reduced payoff amount with lenders, often after default. This option can significantly reduce total debt but comes with serious credit consequences.

Key Risks of Settlement

- Negative credit score impact

- Possible tax liability on forgiven amount

- Limited availability for federal loans in good standing

In short, settlement is a last-resort option and should only be considered after reviewing federal forgiveness alternatives.

When 20-Year Forgiveness May NOT Be the Best Strategy

Forgiveness may not be ideal for borrowers with small balances, high income growth, or strong ability to repay loans quickly.

Although forgiveness sounds appealing, it is not always the most cost-effective path. Some borrowers may save more money by paying loans off faster instead of stretching repayment over decades.

Situations Where Forgiveness Might Not Be Ideal

- Small total loan balance

- Rapid salary growth expected

- Ability to make higher monthly payments

- Desire to eliminate debt quickly for financial freedom

In these cases, aggressive repayment may reduce long-term interest and eliminate debt years earlier than forgiveness timelines.

So the bottom line is: Forgiveness is powerful, but not always financially optimal for borrowers who can repay quickly.

Strategic Decision Framework: Choosing the Best Repayment Path

The best strategy depends on income trajectory, loan balance, employment type, and long-term financial goals in the United States.

To simplify decision-making, borrowers should evaluate their repayment strategy using four core questions:

1. What Is My Expected Income Growth?

Higher future income may reduce the value of long-term forgiveness.

2. Do I Qualify for PSLF Employment?

If yes, 10-year forgiveness may be better than waiting 20 years.

3. Is My Loan Balance Large Relative to Income?

Large balances often benefit more from IDR forgiveness programs.

4. Do I Want Payment Flexibility or Fast Debt Freedom?

Flexible payments → IDR forgiveness

Fast payoff → refinancing or aggressive repayment

In short, the optimal repayment path varies per borrower and should align with income stability, career plans, and debt size.

- PSLF offers forgiveness in 10 years for public service workers

- Consolidation can unlock eligibility for IDR forgiveness

- Refinancing may reduce interest, but removes federal protections

- Settlement is a high-risk last-resort option

- Forgiveness is not always best for high-income borrowers

Frequently Asked Questions: Federal Loan Forgiveness After 20 Years

Can federal loans be forgiven automatically after 20 years?

No. Federal loans are not forgiven automatically after 20 years. Borrowers must be enrolled in an Income-Driven Repayment plan and complete 240 qualifying payments before forgiveness is granted.

In short, forgiveness requires verified qualifying payments—not just waiting 20 calendar years.

Do income-driven repayment plans guarantee forgiveness?

Yes, IDR plans provide a pathway to forgiveness, but only after meeting eligibility requirements, maintaining enrollment, and completing qualifying monthly payments.

Here’s what matters: IDR plans lead to forgiveness only if all program rules are consistently followed.

What happens if I miss payments during the 20 years?

Missing payments can delay forgiveness because only qualifying payments count toward the 240-payment requirement under federal repayment programs.

So the bottom line is: Payment consistency is critical to reaching forgiveness eligibility on time.

Will my remaining loan balance definitely be canceled?

Yes, if you meet all IDR requirements, the remaining federal loan balance can be forgiven after completing the required repayment timeline.

In short, cancellation occurs only after successful completion of all qualifying payments and eligibility verification.

Are forgiven federal student loans taxable in the United States?

Federal student loan forgiveness is currently tax-free under temporary federal provisions, but future tax treatment depends on legislative changes.

Here’s what matters: Tax treatment may change, so borrowers should plan for possible future tax implications.

Reddit/Quora Style User Questions

Is waiting 20 years for student loan forgiveness worth it?

It depends on income growth, total loan balance, and long-term financial goals. High-balance, low-income borrowers benefit most from forgiveness strategies.

Can I switch repayment plans and still qualify?

Yes, but switching plans incorrectly may reset qualifying payment counts or delay forgiveness eligibility depending on federal policy adjustments.

Final Decision Guide: Should You Wait 20 Years for Loan Forgiveness?

Waiting 20 years for forgiveness is best for borrowers with high balances, lower income growth, and a need for flexible payment protection.

Choosing whether to rely on long-term forgiveness requires evaluating both financial and lifestyle goals. Some borrowers gain maximum benefit, while others may save more by paying loans faster.

Quick Decision Framework

| Borrower Profile | Best Strategy |

| High debt + low income | 20-year IDR forgiveness |

| Public service career | PSLF (10-year forgiveness) |

| High salary growth | Faster repayment or refinancing |

| Financial hardship | IDR forgiveness or settlement evaluation |

So the bottom line is: Forgiveness is ideal for long-term affordability, but faster repayment may reduce total interest costs.

Final Takeaway: The Truth About 20-Year Federal Loan Forgiveness

Federal student loans can indeed be forgiven after 20 years—but only under specific Income-Driven Repayment programs. Forgiveness is not automatic, requires consistent qualifying payments, and depends on loan type, repayment plan, and federal policy stability in the United States.

Borrowers who carefully maintain IDR enrollment, recertify income annually, and avoid payment interruptions can successfully reach loan cancellation eligibility.

However, forgiveness is not the best option for every borrower. Those with high earning potential or small loan balances may benefit more from aggressive repayment strategies instead of waiting decades.